Financial product advertising guidelines in Australia

Updated: 6 January 2020

Here’s a guide for what you need to know when advertising your financial products in Australia.

It's useful to note that the approach in Australia has been to include advertising guidelines for ICO’s and crypto assets under an existing regulation; in this case, regulation 234 - advertising financial products and services.

So, as you read, remember that that these guidelines apply to traditional financial products and ICO’s.

And, the Australian Securities and Investments Commission (ASIC) enforces compliance with the guidelines outlined in this article.

In a hurry? Jump ahead.

Your advertising objective

Regardless of your financial product or service type, clear, accurate and balanced message should be your advertising objective for financial products and services.

The minimum requirement vs best practice

The minimum requirement is for you to avoid a misleading and deceptive conduct claim.

Your best practice approach involves you helping consumers make decisions with the content you supply.

Coverage - regulation 234 guide - advertising financial products and services

So who is covered by the regulation? Regulation 234 applies to:

- Promoters of financial products;

- Financial advice services;

- Credit products and credit services; and

- Publishers of promotions about these products and services.

Also, distributors and agents are covered by reg 234.

All communication channels covered

All methods of informing consumers or promoting financial and credit products and services are covered.

So this means - magazines and newspapers, radio, TV, outdoor ads, internet ads, social media, telemarketing, text messages etc.

Disclosures and guides

Statements in Product disclosure Statements and Financial Service Guides are not included in the meaning of advertising.

ASIC’s regulatory guide

If your advertisements do not meet ASIC’s good practice guidance, here are the actions ASIC can take:

- Gather information e.g. issue a substantiation notice

- Issue a stop order or seek an injunction to stop continued advertising or an associated disclosure document

- Issue a public warning notice

- Cancel a promoters AFS licence or credit licence, or vary its conditions.

Testing your advertisement

When testing your advertisement, ASIC encourages you to test that your advertisement:

- Is accurate and balanced; and

- Does not create a misleading or deceptive impression in the mind of an ordinary and reasonable member of the advertisement’s audience.

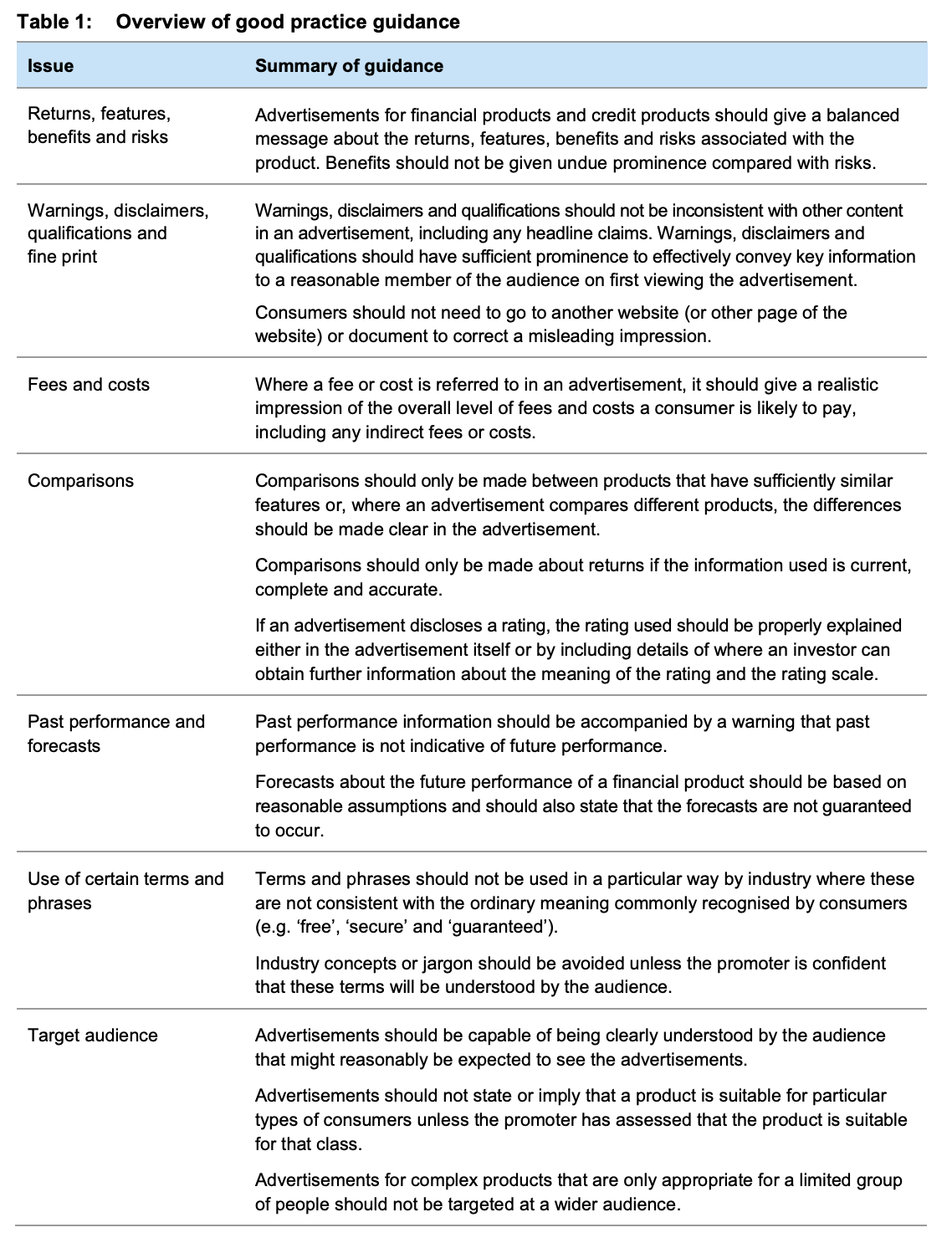

Good practice criteria

Below are the specific criteria for good practice advertising of your ICO or crypto assets.

Returns, features, benefits

The key word for this best practice guideline is ‘balanced’ - this means your advertisements should give a balanced message about returns, features, benefits and risks of your product. Yes, and this includes your ICO's.

In practical terms, don’t overstate the potential benefits or create unrealistic expectations.

Also, along with benefits, advertisers should include a statement about risks associated with a benefit or about a product generally.

I'm going to use some ICO examples because they are not explicitly covered in reg 234.

Example: ICO potential returns

If you are going to advertise an expected rate of return on the sale of a coin, you should also state that the expected return may not arise, and that the investor’s balance may even fall.

Other return, feature, benefit and risk guidelines:

- Multiple offers - If some benefits are mutually exclusive (e.g. 2 offers that cannot be taken up simultaneously), this should be made clear in the advertisement.

- Open ended promises - clarify that a benefit may change if circumstances change e.g. a reduction in the rate of return etc.

- Reasonable time - your feature or benefit should remain available for a reasonable time given the nature of the market and the nature of the advertisement.

- Foreign currency - you should make it clear if returns are calculated in a foreign currency. For example if you are an Australian company offering an ICO and calculating potential benefits and value increases in USD.

Risks

You should make sure that risks about your financial product are clear, not hidden or difficult to understand.

Example: understating risks of trading software

If you have set up software that helps consumers track and purchase cryptocurrency, you should avoid marketing material that makes statements like these:

- Cryptocurrency trading is easy; or

- Returns of 5-10% per month and returns of 60-120% per year can be consistently achieved.

Refunding customers that have made software purchases from you is a likely consequence if ASIC finds you are in breach of this guideline.

Also, you should be careful not to:

- Guarantee the safety or security of a financial product because there are very few products that can claim they are fully insured or guaranteed.

Example: loans to trade cryptocurrency

You should avoid any statements about loans for cryptocurrency trading being ‘stress free’ strategies to accelerate your wealth. This is because there are risks involved in gearing to invest in cryptocurrency which would make it unlikely that any strategy like this would be ‘stress-free’.

Warnings, disclaimers, qualifications and fine print

An advertisement won’t always include in its headline claim all information about the product that’s relevant to a consumer decision.

So, when you have a headline with benefits about an ICO, you’ll need to include qualifications about the benefits as well to balance the information in the headline claim.

Also, your warnings, disclaimers and qualifications should not be inconsistent with other content in your advertisements including headline claims.

Also, you cannot get away with referring a consumer to another website or web page or documents such as a PDS, prospectus or contract - these won’t be sufficient steps to correct a misleading or deceptive headline claim. We know this from the case of the internet company TPG - Australian Competition and Consumer Commission v TPG Internet Pty Ltd [2011].

Fees and costs

You’ll need to give consumers a realistic idea of the overall level of fees and costs a consumer is likely to pay.

In practical terms this means, don’t say that there are no fees if there are fees but they are waived only if certain criteria is met.

Also, there’s a difference between fees and costs, so don’t include fees and forget about costs or vice versa.

So, this means including the impact of fees and costs on returns for financial products.

Below are some examples.

- Returns should be net of fees and costs to the greatest extent practicable

- If a fee level is variable, the maximum fee should be deducted from the possible returns

- Where it’s impractical to deduct some fees or costs, the existence of undeducted fees or costs should be disclosed

- Where practicable, the size of undeducted fees and costs should be disclosed

- Where a product is offered with multiple fee options, advertised returns should make clear which fee option they relate to; and

- Where a scenario is given for a specific investment period, entry and exit fees should be deducted.

Fees for financial advice services

You should not state that an advice service is ‘free’ or ‘low cost’ if the consumer would pay for the service indirectly through the fees and costs of any financial products.

Interest rates

Under the national credit code, you don’t need to include an interest rate. But, you’ll need to include the rate if the advertisement states the amount of any repayment.

Also, you’ll need to include any fees and charges.

Example: comparison advertising discounted interest rate

Don’t tell consumers they’ll save on interest for a home loan compared to a competitor if this saving wont apply to all customers.

Other useful guidelines:

- Initial promotion period - if there’s an initial promotional period for an interest free offer, state this; and

- After promotion rate - if the interest rate revert to a standard variable rate after the promotion period, include this information.

Comparison rates

A comparison rate helps consumers identify the true cost of a loan.

So, it needs to include the interest rate, fees and charges relating to a loan. This includes an annual fee to access a loan.

If this information is not included, consumers could be mislead.

Also, the comparison rate must not be less prominent in an advertisement than any interest rate or the amount of any repayment.

Display guidelines

Below are examples of less prominent comparison rates, and in breach of section 164 of the National Credit Code.

- Faded colour, smaller size font compared to the interest rate

- Additional click or step to view the comparison rate

- Location of the comparison rate is easy to overlook

Accuracy warning

You’ll need to include a warning that the comparison rate is only accurate for the example in the advertisement. And, the warning will need to be in the same form as the comparison rate (e.g. spoke or written form).

For online banner ads - you can include a clear link or reference to the warning. The language should be clear.

Comparisons

Below is guidance for different types of comparisons.

Comparisons between products

When comparing products, the products should have sufficiently similar features to make the comparison relevant and not misleading.

In practical terms, this means you should not:

- Compare debentures to bank term deposits with a statement like ‘is your money earning x% in a bank term deposit?’

- Compare an insurance policy based on the premium but not the excess.

Comparison of benefits and returns

Consistent with other parts of reg 234, a comparison of benefits and returns should be accurate, balanced and have a reasonable basis.

This especially includes using terms like ‘high’ and ‘low’ to compare benefits or returns.

Ratings

Credit ratings should only be advertised to retail clients if the rating is issued by a credit rating agency that’s authorised under its AFS licence to provide financial advice to retail clients.

Ratings may include credit ratings, ratings, recommendations and opinions produced by financial product research houses.

The rating should be properly explained either in the advertisement or by including details where an investor can obtain further information about the rating.

Also, if you are going to use ratings, you’ll need to include this statement:

Ratings are only one factor to be taken into account when deciding whether to invest in a financial product or take up a credit product.

Also, only current ratings should be used.

Awards

The award granter should be identified and the award explained, including the currency of the award.

And if the award is granted by someone related to the promoter, this should be mentioned.

Past performance and forecasts

If you are referencing past performance, you’ll need a statement like this one:

Past performance is not indicative of future performance.

And for any forecasts, you’ll need reasonable grounds for such representations and they must not be misleading.

Terms and phrases

Be careful when using these terms: free, secure and guaranteed. You’ll need to take this precaution to avoid situations where you:

- Create expectations that cannot be met;

- Indicate a level of security that does not exist; and

- Mislead about different levels of protection and risk.

Debenture example

In practical terms, if you are issuing a debenture, don’t use the phrase ‘invest with certainty’ and ‘the rate you choose if secured for the term of your investment’.

Terms prohibited by the Corporations Act

You should not use these terms:

- ‘Independent’, ‘impartial’, ‘unbiased’ where a person receives a commission, volume bonus or other benefit

- The terms ‘stockbroker’, ‘sharebroker’, ‘insurance broker’, ‘general insurance broker’ and ‘life insurance broker’ should not be used if a person is not authorised by an AFS licence to use those terms.

An example where there’s no independence - a financial advisor that gets commission from the financial products they recommend.

‘Financial counsellor’

This term should only be used for a service that:

- Helps people in financial difficulty

- Has no fees or charges payable by the client

- Np pay is payable to the financial counselling agency in relation to any action of the client.

Endorsements and testimonials

Only genuine endorsements and testimonials are allowed.

Target audience

Promoters need to consider the characteristics of the audience that will see the ad.

For example, their:

- Financial literacy

- Knowledge

- Demographics

And, while the promoter’s target audience may be different to the actual audience, the actual audience needs to be taken into account.

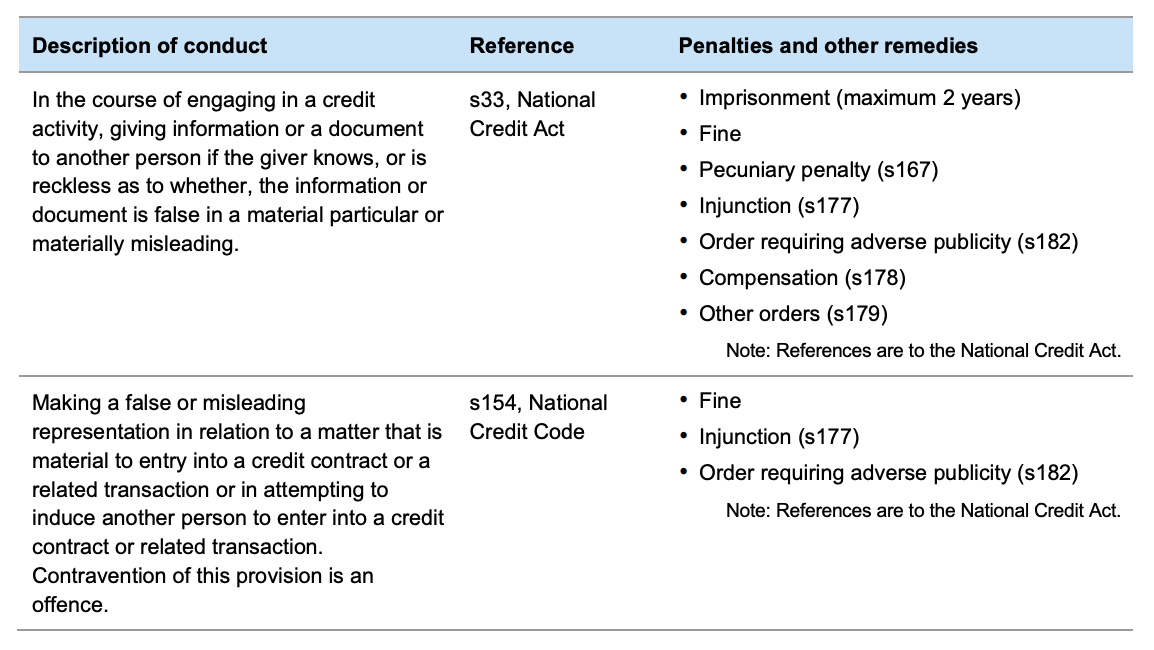

Responsible lending

The key principle for responsible lending is that credit licensees must not enter into a credit contract with a consumer that’s not suitable for them.

This is judged on the consumer’s requirements, objectives and their financial situation.

So, you should be careful with ‘no-doc’ type products, ‘instant’ or very fast approval or even approval with ‘no credit checks’ because these features may not be consistent with the obligations of a responsible lender.

Also, take care when advertising a product is suitable for a particular class e.g. consumers that have been knocked back by other credit providers or students.

These are terms you should not use: ‘guaranteed acceptance’, ‘pre-approved’ because you’ll need to follow an independent assessment when an application comes through.

Guaranteed finance example

ASIC stopped an advertisement that said ‘no application refused’ because its misleading, because of responsible lending principles of checking suitability.

Credit limit increases

Card issuer’s cannot send unsolicited invitations for credit limit increases unless the customer has previously consented to this - National Credit Act, s 133BE-133BF.

Complexity

Your ad should be simple and easily understood by the audience likely to see it.

If you have a complex product, then you should not advertise if in a limited space like internet benners, 30-second TV ads.

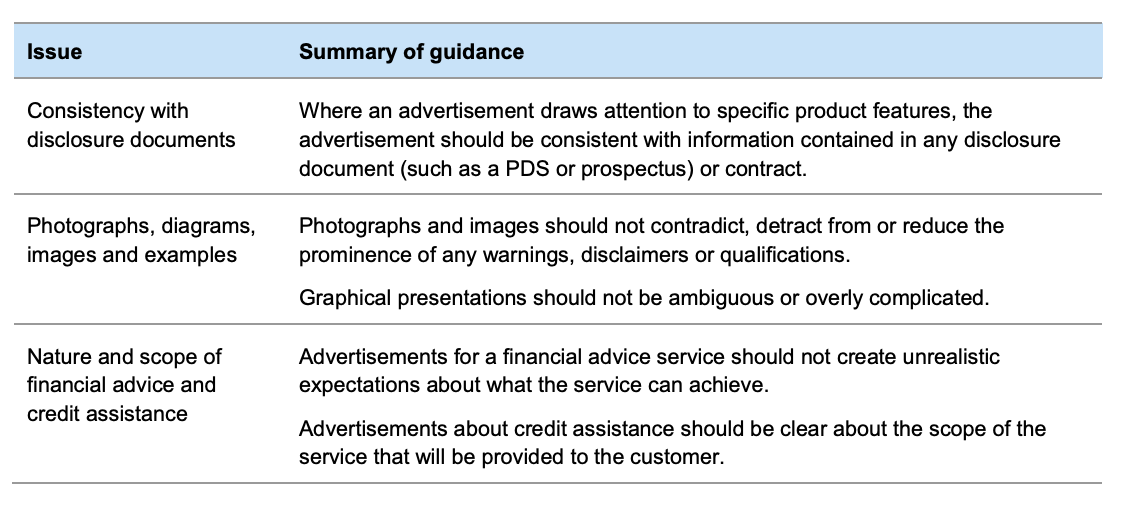

Consistency

Your ad should be consistent with any disclosure document like a product disclosure statement, financial services guide or prospectus.

Example: credit card guarantee

A promotional campaign should not contain a guarantee that an interest rate will stay low if the terms in a credit contract state that the interest rate can be raised at any time.

Financial product advertisements must include a statement like this one:

“You should consider the PDS or prospectus in deciding whether to acquire this product” - and indicate where the PDS or prospectus can be obtained - section 734 and section 1018A of the Corporations Act.

Photos, diagrams, images and examples

Your images should not detract from or reduce the prominence of qualifying statements.

So, in practical terms, you should be careful when using images associated with success, wealth, safety and security.

In practical terms this means...

For a funeral insurance ad - do not use images of an older audience, if a low price will only apply to younger customers.

Keeping things simple is important.

This means, tables, diagrams, graphs, charts and maps should be easy for consumers to understand.

Practical application of this guideline would be keys for complex diagrams and graphs, and time periods that fairly represent the information and do not give skewed outputs.

Nature and scope of financial advice and credit assistance

The key principle here is - don’t create unrealistic expectations about what a service can achieve.

For example, don’t say that an advisor will consider all all relevant products across a market if this won’t occur.

Also, don’t describe an advice service as offering ‘full financial plans if the advisor can only advise on a narrow range of issues.

The same principle applies for not misrepresenting an advisors experience or qualifications.

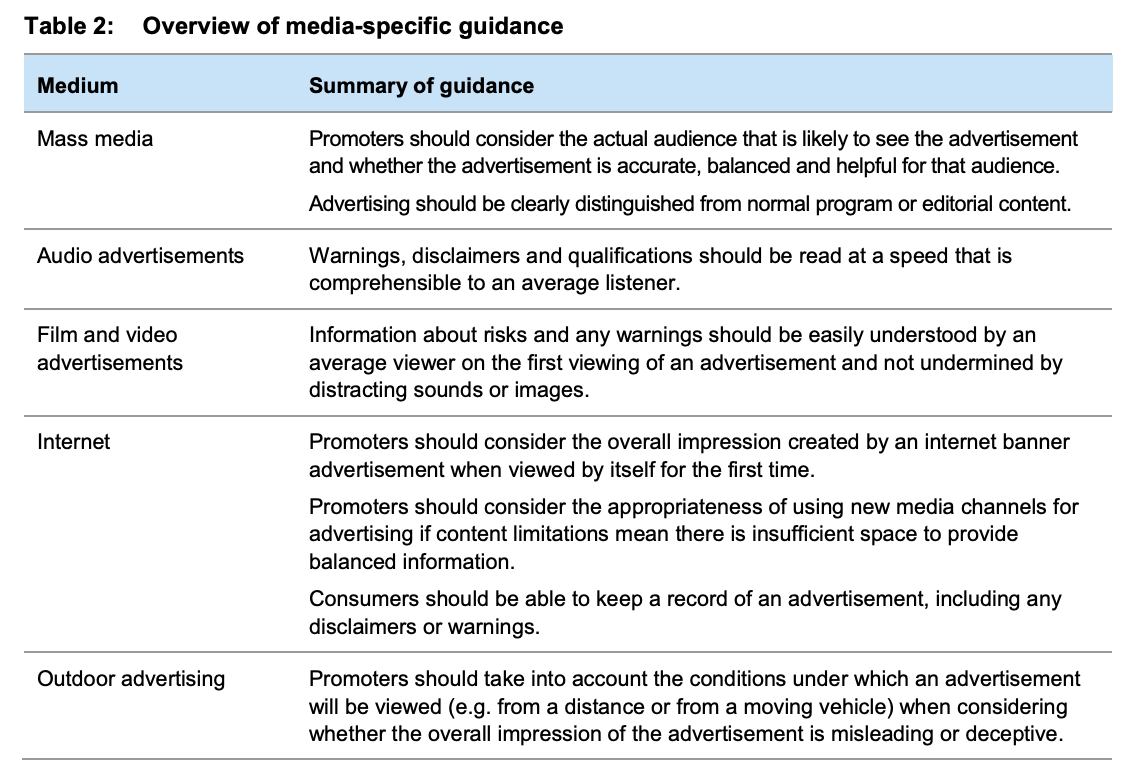

Media specific guidance

ASIC has guidance for mass media, internet and outdoor ads.

Let’s start with mass media.

Mass media

First, mass media includes radio, TV, newspapers, magazines and the internet. It has the capacity to reach a wide audience.

Ads should not be presented as news programs or other programs.

Practically, this means a radio presenter needs to disclose if a promotion is an ad before they read the ad.

Also, this is particularly important in the context of ‘high trust’ environments like blogs or social media blogs.

Audio ads

Warnings and disclaimers need to be read at a speed that’s easy for an average listener to understand. This also applies to telemarketing.

Film and video ads

Warnings and disclaimers need to be prominent in film and video ads. And, an average viewer should be able to easily understand any disclaimer or conditions.

Internet ads

Internet ads like webpages, banners, videos on YouTube etc need to allow additional information.

For example, internet banners with strong headline claims need to balance these headlines with information about the risks.

Also, consumers should be able to keep information about disclaimers in case a dispute arises. So you should not just rely on a disclaimer that scrolls by quickly.

Outdoor ads

Billboards, posters, signs in public venues and aerial display all count as outdoor ads.

This type of advertising may be more appropriate for branding rather than conveying important complex information about a product.

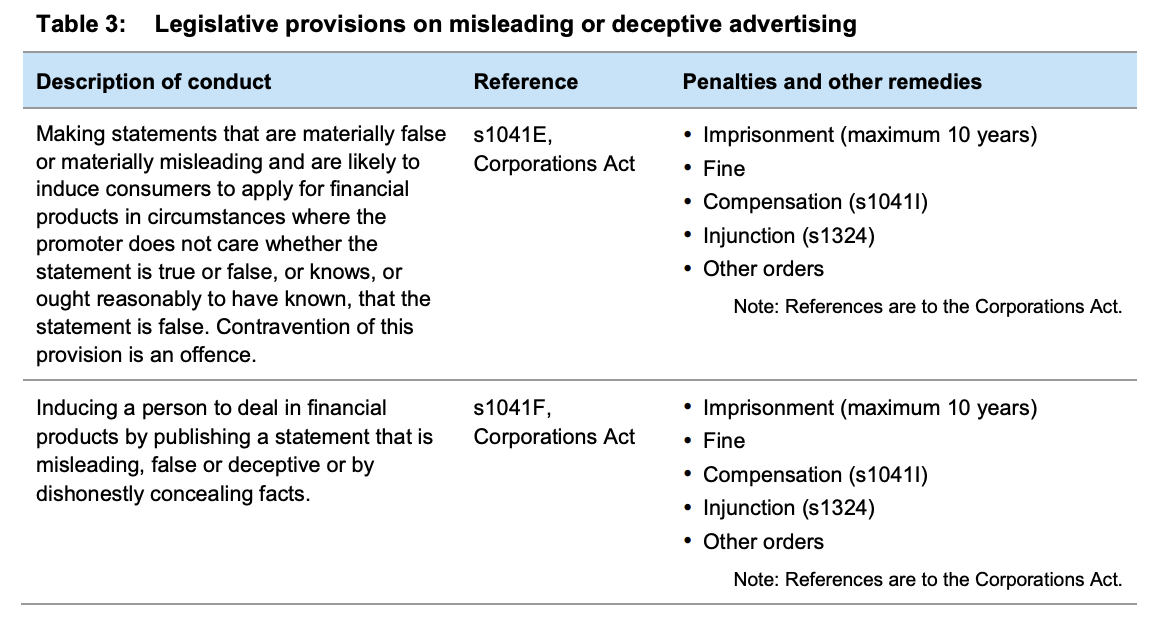

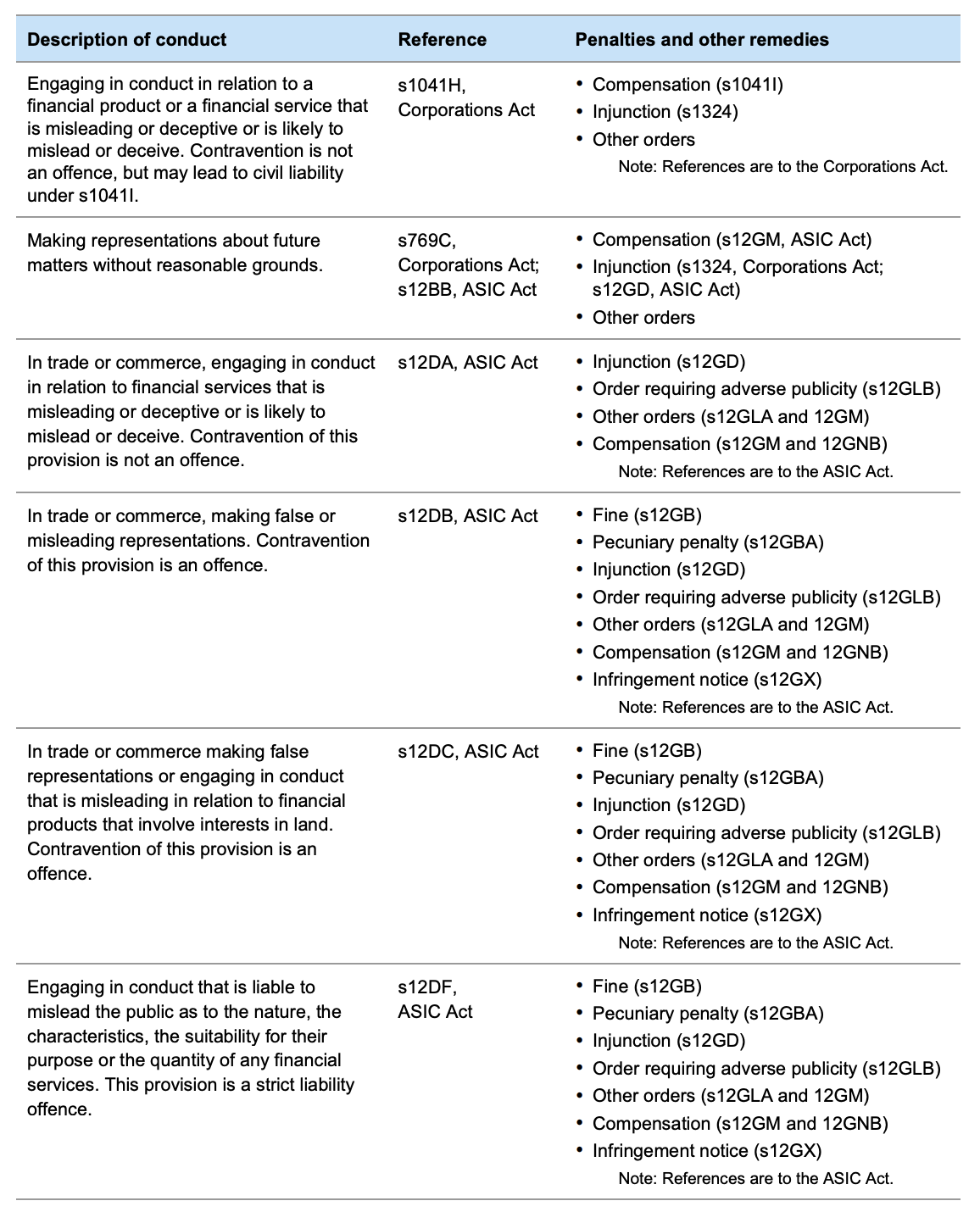

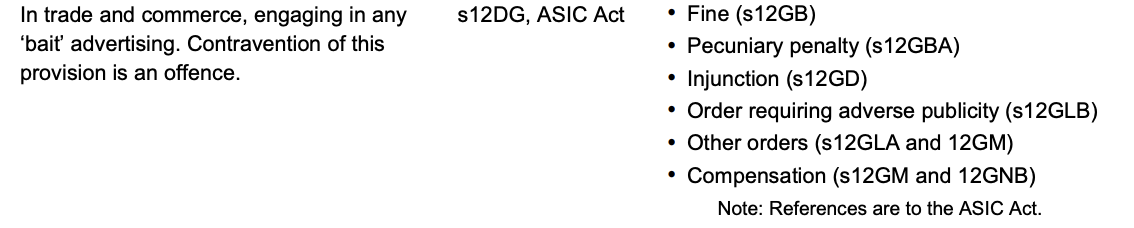

ASIC’s regulatory powers

Below is what you need to know about the consequences that may follow for misleading or deceptive conduct.

How ASIC assess ‘misleading and deceptive’

Below are the factors that ASIC takes into account when assessing if your ad is misleading or deceptive.

- the subject of the advertisement;

- the content of the advertisement;

- the format of the advertisement;

- the audience that will view the advertisement;

- the media used to communicate the information; and

- the likely effect of the advertisement.

ASIC’s criteria for financial and credit product ads

ASIC will ask if the ad is:

- Clear and accurate

- Balanced

- Descriptive of risks, fees and other draw backs

- Capable of being advertised in a clear and simple way.

ASIC’s criteria for financial advice or credit assistance

ASIC will check if the ad:

- Creates realistic impressions

- Includes limitations of the advice or assistance to be given

- Has costs that are realistically estimated

- Has claims about impartiality, that they are true.

Key principles about what’s misleading or deceptive

These legal principles apply:

- Intention to mislead or deceive is irrelevant;

- Consumers don’t actually need to have been misled;

- Ordinary and reasonable member of the audience’s audience is the bench mark;

- The audience is the audience that’s actually reached;

- The overall impression on the first run is important;

- Qualifications for a headline claim must be clear and prominent;

- Promoters cannot rely on an accurate disclosure document to undo the effect of a misleading statement; and

- Silence can also be misleading.

ASIC’s approach for contraventions

Examples of things ASIC can do if there is a contravention (and this list is not exhaustive):

- Gather more information before taking regulatory action;

- Seek an injunction to stop the ad;

- Issue a stop order on disclosure documents;

- Seek compensation for the impacted investors;

- Seek an order to to redress loss suffered by non-party consumers;

- Accept an enforceable undertaking (your promise to do/not do something, where a breach will have consequence);

- Seek criminal charges;

- Issue a public warning.

ASIC’s approach with depend on the provision that’s been breached.

Publishers and media outlets

While primary responsibility for an ad rests with the organisation placing the ads, the publisher is also responsible.

Defence for publishers

Publishers can defend themselves by claiming they did not know or had no reason to believe the publication would be an offence: section 1044A, Corporations Act and section 12GI(4) ASIC Act.

What ASIC expects from publishers

ASIC expects the following from publishers:

- To cease publishing an ad that’s subject to a stop order or public warning notice.

- A defence won’t apply to publishers that have contributed to the cotnent of an advertisement e.g. in writing advertorials or if they otherwise have an active invovelment in the promotion of a product or service like via co-branding.

Aggregators and comparison sites

Aggregators or comparison sites have the primary role of comparing or raking products.

Below are the responsibilities of aggregators and comparison sites:

- Disclose links to the providers of the products being compared including commissions, referral fees, payments for inclusion in comparisons and featured products

- Warning if not all providers are included in the comparison

- Ads should be clearly displayed as ads

- A warning that products compared do not compare all features